9 April 2026

Amazon’s Big Spring Sale Grew 3% YoY Even as Discounts Softened

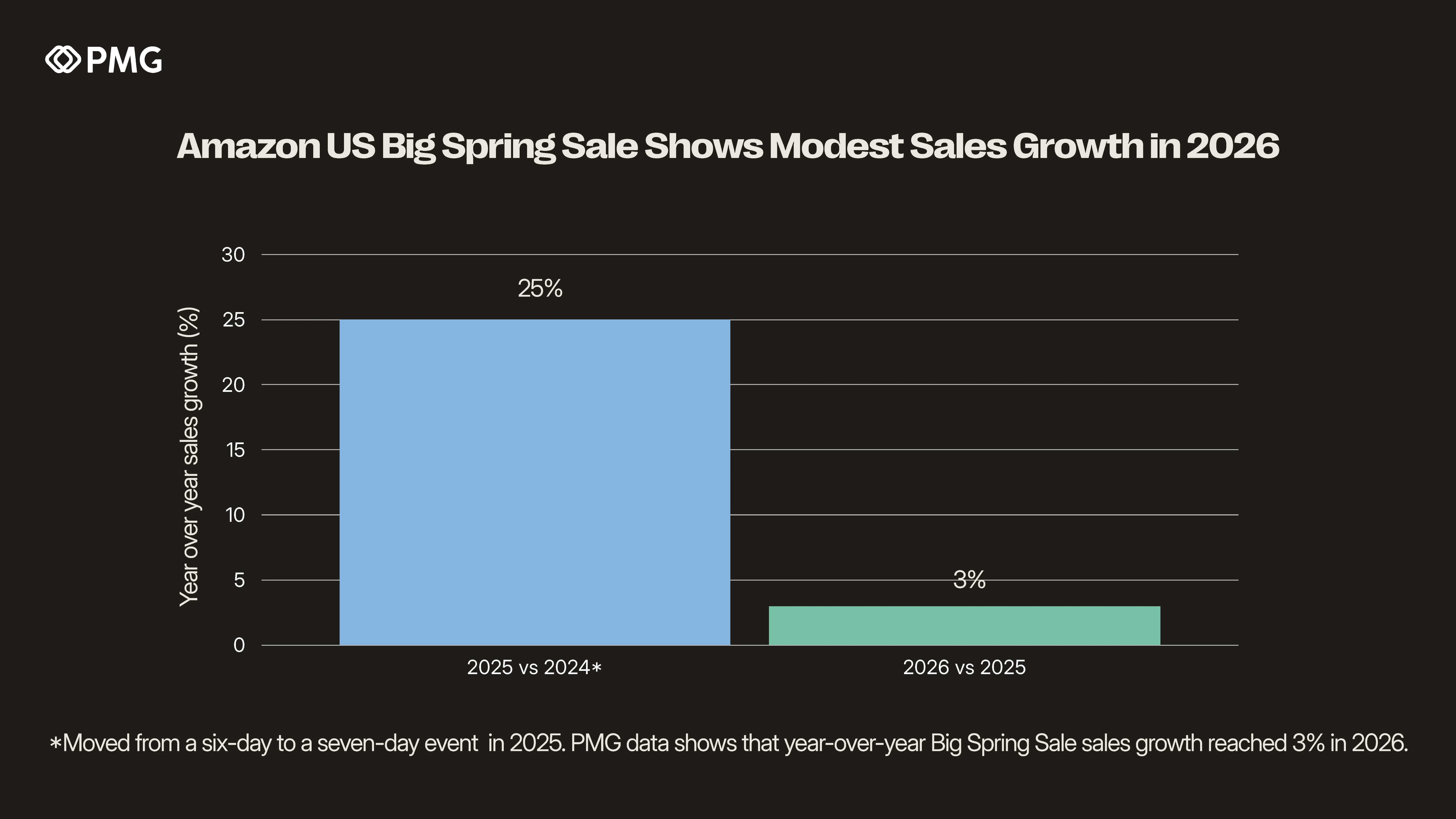

Amazon’s 2026 Big Spring Sale delivered modest year-over-year growth, underscoring that shopper demand around tentpole promotional moments remains resilient even as discounting becomes less aggressive. PMG data shows that average sales on Amazon US during the 2026 event rose by 3% versus the 2025 Big Spring Sale, a marked deceleration from the just over 25% increase in sales between 2024 and 2025, when the event moved from a six-day to its current seven-day length.

A Strong Event Despite Lighter Discounting

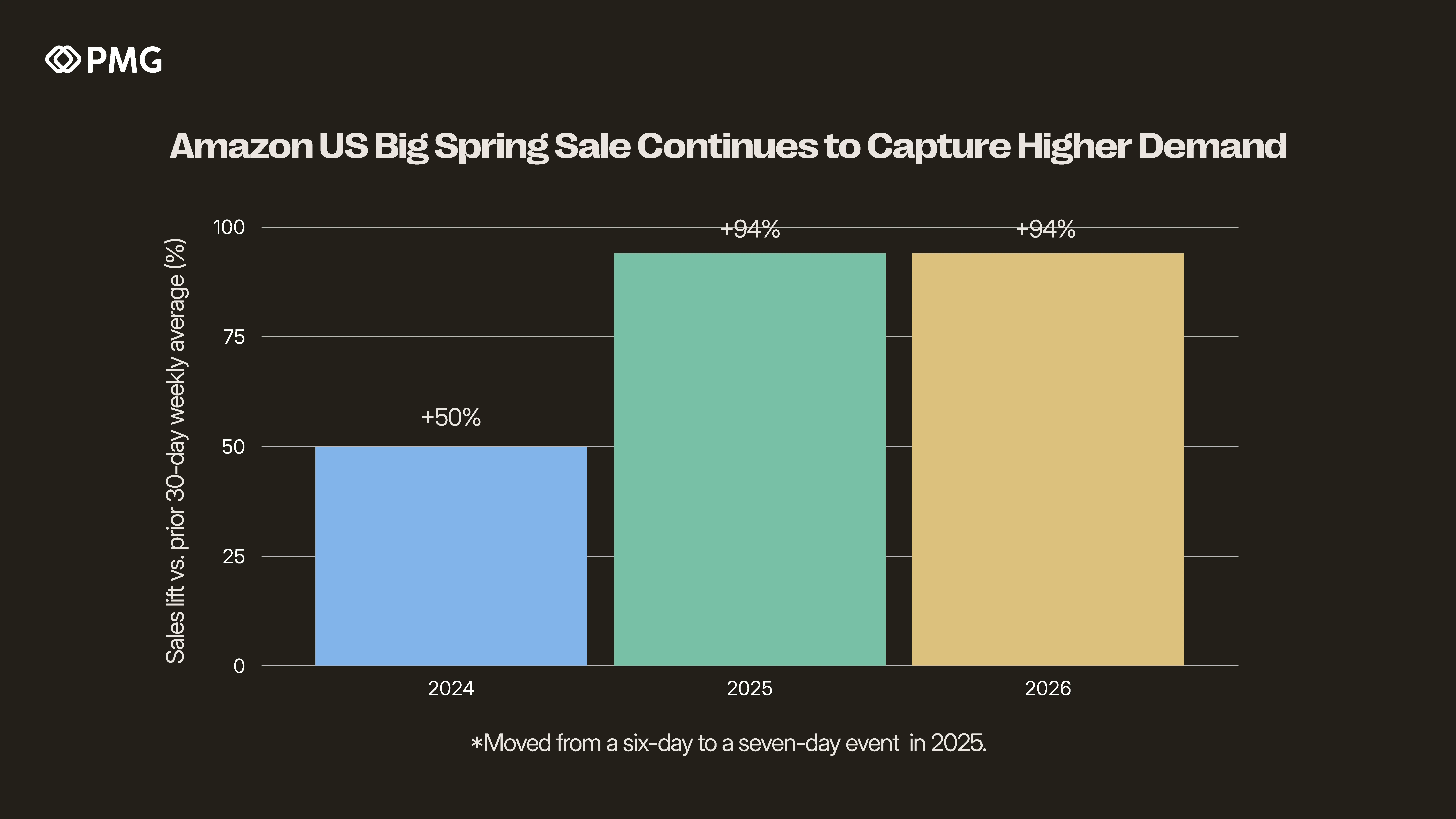

The event still captures a larger share of consumer demand than a typical week. Average sales during the seven-day sale were 94% higher than the prior 30-day weekly average, the same rate observed in 2025, and well above the 50% figure from the six-day event in 2024. That pattern indicates shoppers are continuing to concentrate spend around known promotional periods, even when deals are not as deep as they once were.

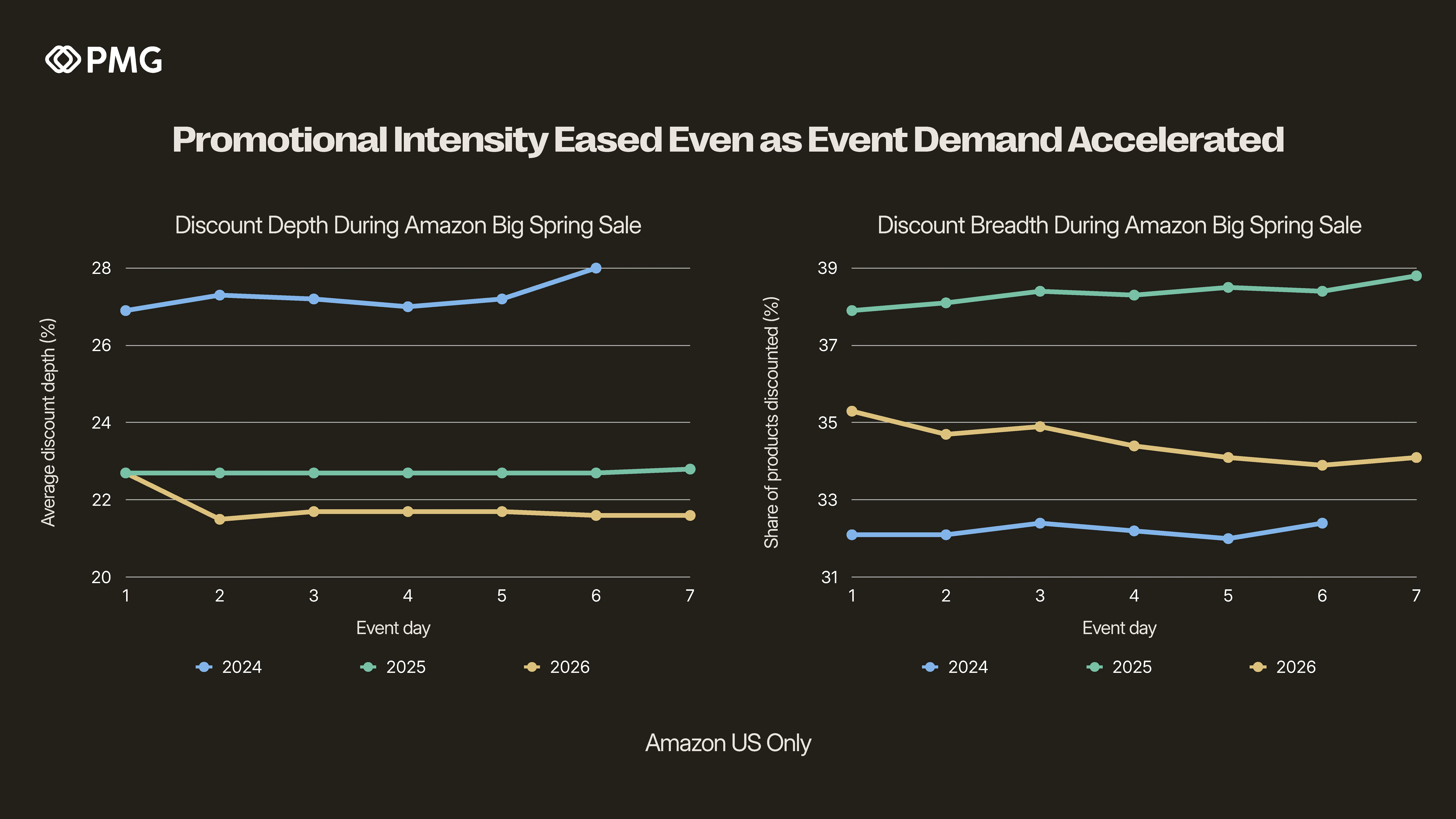

That latter point is what makes this year’s results especially notable. Across Amazon US, average discount depth during the 2026 Big Spring Sale was slightly below 2025 levels and materially below 2024 levels. After opening at 22.7% on Day 1, average discounts settled slightly above 21.5% for the remainder of the event, compared with an average of 22.7% in 2025 and roughly 27% in 2024. Discount participation was also lower this year. Roughly 34% to 35% of products were discounted on any given day during the 2026 event, trailing the more than 38% observed in 2025.

This broader pattern illustrates that consumers remain highly responsive to the signal of a sales event, particularly in a market characterized by ongoing price sensitivity. Brands may not need to match the deepest discounting levels of prior years to capture demand, but they do need to be visible on the platform, remain competitive, and deliberate about where and how they promote.

Category Trends Tell a More Nuanced Story

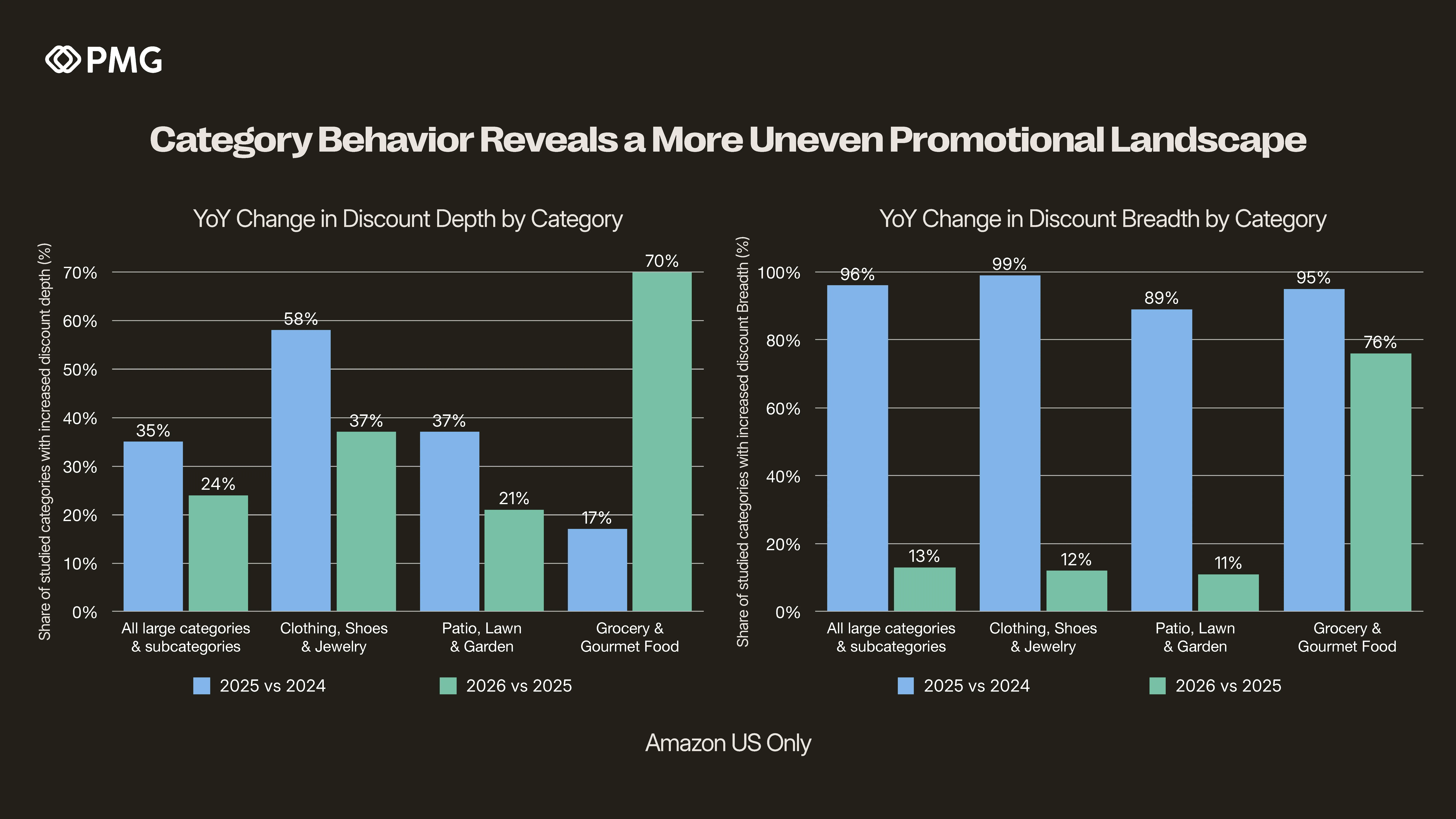

That said, the discount environment was not uniform across categories. Among categories with at least 5,000 unique ASINs observed in each of the 2024, 2025, and 2026 events, only 24% increased average discount depth in 2026 versus 2025, down from 35% in the prior year-over-year comparison. At the same time, only 13% of those categories increased the share of discounted products year-over-year, a sharp decline from the 96% figure seen in 2025 versus 2024.

Grocery & Gourmet Foods stood out as an exception. While categories such as Clothing, Shoes & Jewelry, and Patio, Lawn & Garden broadly mirrored the sitewide decline in discounting, 70% of the studied Grocery & Gourmet Foods categories increased average discount rates compared with the 2025 event. That divergence suggests that essential, food-related categories may remain more promotionally active than other parts of the Amazon marketplace, potentially because price sensitivity is especially acute there and margin pressure may be less severe than in more tariff-exposed categories.

PMG Portfolio Trends Point to a More Mixed Brand-Level Picture

While marketplace-level data points to a relatively strong Big Spring Sale event, PMG portfolio ecommerce performance during this period was more mixed. Across tracked brands, results varied on both a year-over-year and week-over-week basis, continuing a pattern seen across much of 2026. In other words, there is limited evidence that retailers introduced net-new promotions in direct response to the Amazon Big Spring Sale event.

Nearly half of observed brands recorded total site traffic growth during the period, and select brands saw conversion gains, but the impact was not broad-based enough to indicate a clear portfolio-wide lift tied to the event. That more uneven pattern may reflect a range of factors, including category dynamics, differing promotional strategies, and the degree to which brands aligned retail or media activity with Amazon’s event timing. Instead, many brands may already be prioritizing larger seasonal moments later in May and June, when summer sales activity typically becomes more central to their promotional strategies.

Strategic Considerations for Advertisers

The modest growth of the 2026 Amazon Big Spring Sale reinforces the importance of brand readiness and agility for tentpole sales events as demand rises around known promotional windows. Close monitoring of category-level discount behavior will be critical to informing Prime Day planning, promotional pacing, and product-level pricing decisions now and in the future.

In an environment where shoppers remain value-conscious, even lighter discounts can be effective, but only when paired with the right competitive strategy and event visibility. Brands that enter major retail moments with a clear view of category dynamics, promotional pressure, and consumer demand patterns will be better positioned to capture growth without relying on the deepest markdowns.

Methodology

Amazon Big Spring Sale dates are defined as March 20 through 25, 2024 (six days), March 25 through 31, 2025 (seven days), and March 25 through 31, 2026 (seven days).

For sales-related analyses, PMG examined Amazon US sales across a consistent set of customers spanning from February 2024 through March 2026. Any brands without a full slate of sales data in any intervening period between those dates were excluded. Collectively, the brands included in this analysis drive more than $3 billion in annual Amazon gross merchandise value (GMV).

For discount-related analyses, PMG examined over 30 million products on Amazon US cataloged within Velocity, PMG’s proprietary commerce platform. Discount data includes both Big Spring Sale-specific deals and general promotional discounts across the same set of 30 million products.

For category-specific discount analyses, PMG examined Amazon US categories with at least 5,000 unique ASINs observed across the 2024, 2025, and 2026 Big Spring Sale events.