June 24, 2026

Amazon US Prime Day 2026, Day 1: Fewer Deals on the Shelf, but Shoppers Still Find Sharp Discounts

Prime Day 2026 is underway, and a PMG analysis of tens of millions of products on Amazon US shows that while Day 1 discounts are less pervasive than on the first day of the sale event in prior years, the average discount rate for products on sale has held remarkably steady year-over-year (YoY).

That underscores a multi-year trend PMG has tracked across major Amazon US sales events, with brands continuing to treat discounts as a prerequisite for Prime Day participation, but becoming increasingly selective about where and how aggressively they cut prices. With this year's event pulled forward to June 23-26 and a value-conscious consumer navigating an elevated inflation environment, it’s worth watching whether overall discount trends shift as the event continues.

MethodologyDiscount data included in this analysis encompasses both Prime Day-specific deals and general promotional discounts observed by non-logged-in users across more than 30 million products on Amazon US on June 23, 2026. Prior year comparisons relate to July 8, 2025, and July 16, 2024, respectively.

Early Event Discounts Less Pervasive on Amazon US, but Average Rate Largely Holds Steady YoY

The clearest Day 1 story is a divergence between how deep discounts are and how widely they are offered.

Discount depth held steady: The average discount rate on Day 1 came in at roughly 21.0%, essentially flat against the 21.4% observed on Day 1 of the 2025 event (a YoY change of about -2%, or less than half a percentage point). For context, Day 1 of the 2024 event averaged 22.8%, so depth has eased only modestly over two years.

Discount breadth fell meaningfully: The share of products carrying any discount dropped to 24.6% on Day 1 of 2026, down from 29.0% in 2025 and 29.3% in 2024, a decline of roughly 15% YoY, or about 4.3 percentage points.

This dynamic suggests that brands are protecting margin by narrowing the set of items they promote rather than dialing back the headline discount on the items they choose to feature. This may also reflect Amazon's stricter rules regarding qualifications for discount tagging during Prime Day. For the 2026 event, the retailer instituted longer look-back windows, meaning that products that ran Father’s Day or even Big Spring Sale promotions needed to meet even deeper discount thresholds to qualify for Prime Day Deals, rates that may be infeasible from a margin perspective. For shoppers, the net effect is that the deals are still there, but they are spread across a smaller subset of products.

More Discounts Are Below 20% Off Compared to Prior Years

Looking at the distribution of discount offers by depth, the mix has shifted toward shallower price cuts.

The share of discount offers in the 10% to 19% off band rose to 37.0% on Day 1 of 2026, up from 32.2% in 2025 and 28.0% in 2024, a steady, multi-year climb.

At the deep end, 50% off or more offers now make up just 5.6% of discounts, down from 8.7% in 2024 and roughly in line with 2025's 5.8%.

The 20% to 29% off band—historically the single largest group—slipped to 39.9% from 42.9% in 2025, while the 30%-39% and 40%-49% bands held in the low-to-mid single digits and low teens, respectively.

The takeaway is that the "typical" Prime Day deal is getting shallower. Where shoppers in prior years were more likely to encounter a 20%-plus markdown, a growing plurality of this year's offers cluster in the 10%-19% range.

For brands, that shift emphasizes how much clear messaging, comparison-friendly pricing, and search visibility matter when raw discounts themselves are more modest.

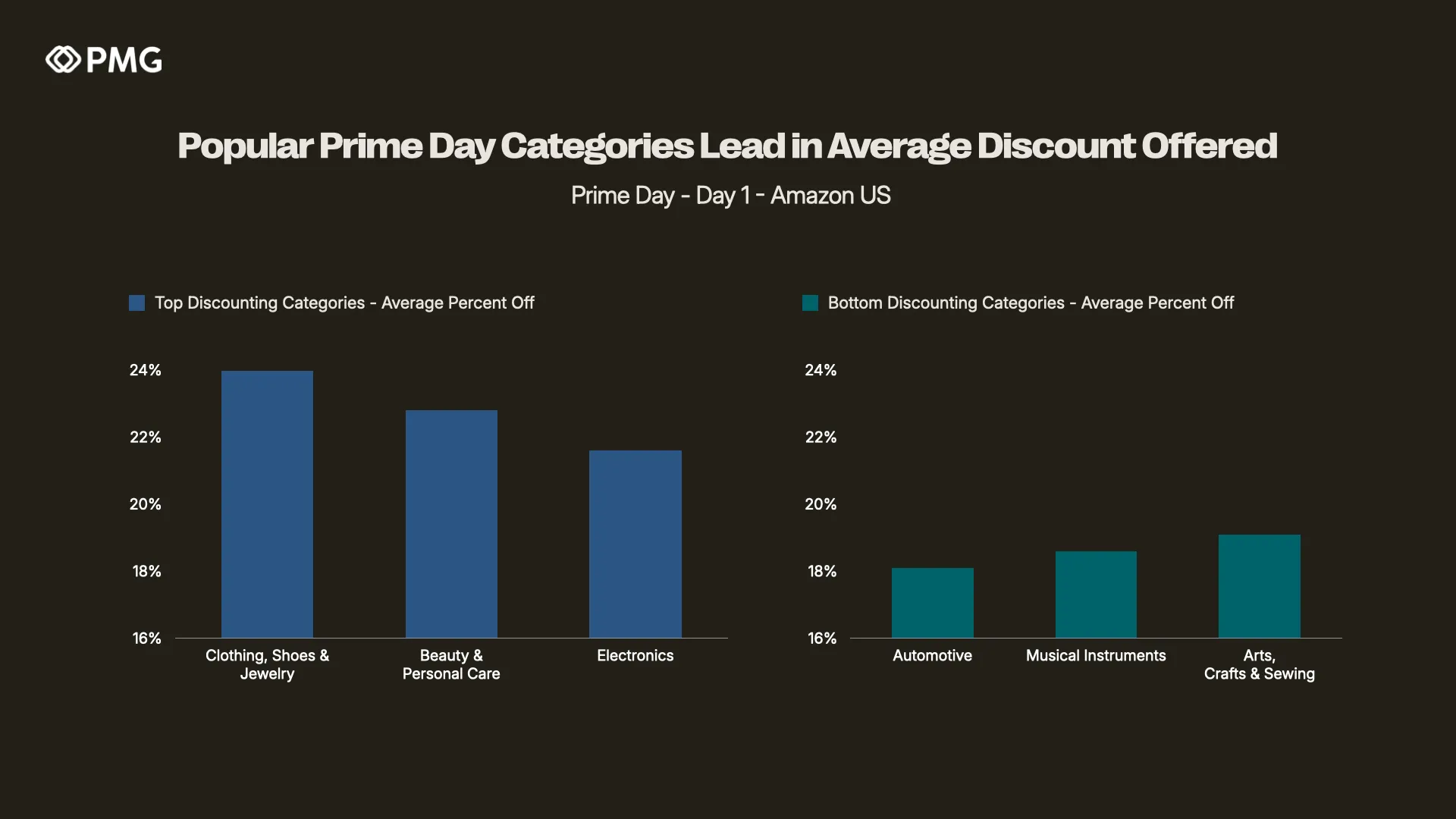

Popular Prime Day Categories Lead in Average Discount Offered

Not all categories are discounting equally on Day 1. The most aggressive markdowns are concentrated in the categories most associated with Prime Day demand.

The split is intuitive: high-consideration, gift-able, and replenishment-driven categories—apparel, beauty, and electronics—are leaning into Prime Day with the deepest average cuts, while more niche or need-based categories like automotive and musical instruments are holding back. For advertisers, this reinforces that competitive context is category-specific; a 20% discount that stands out in one category may be table stakes in another.

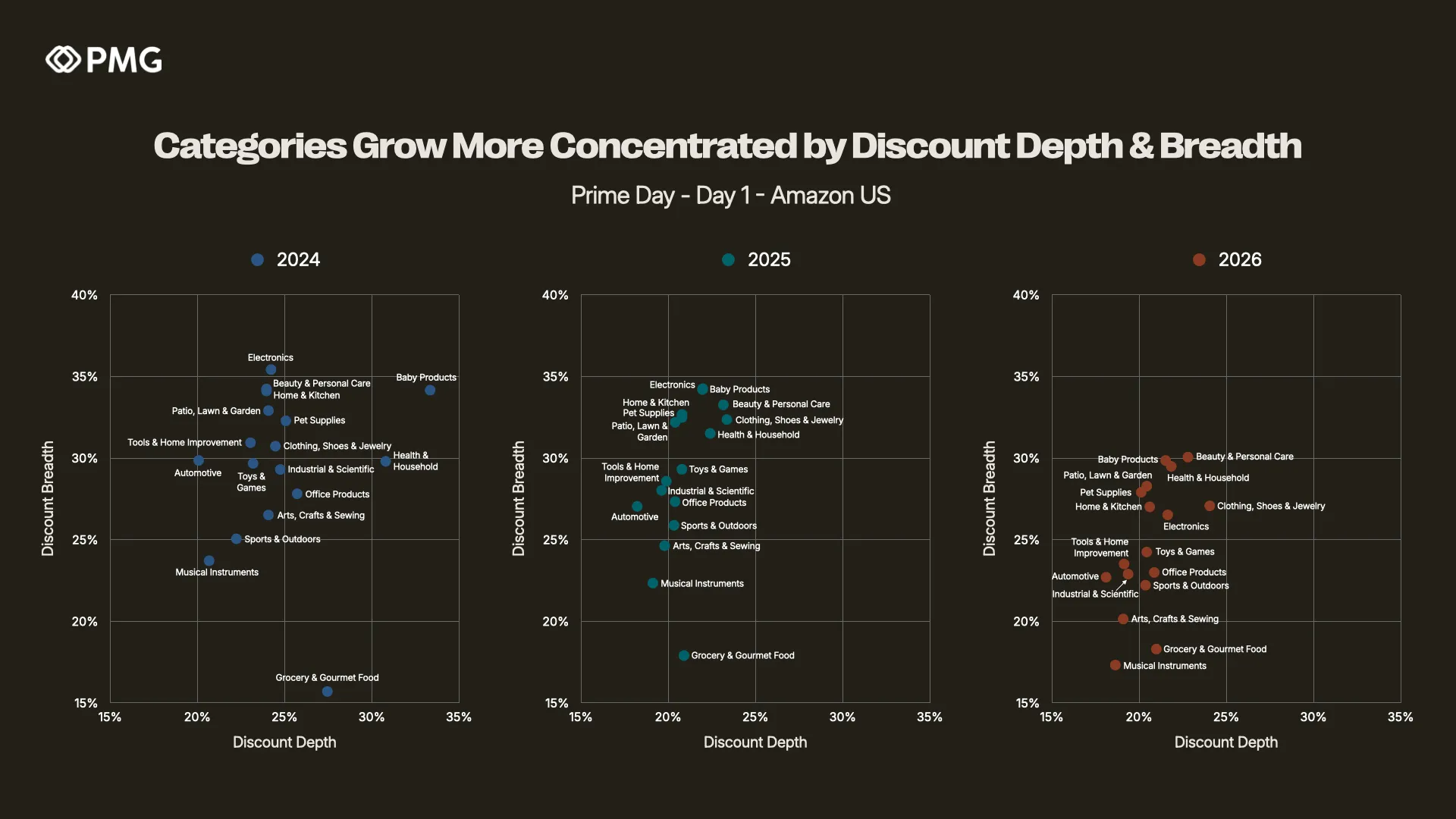

Categories Grow More Concentrated by Discount Depth & Breadth

Beyond the whole-site averages, the category-level picture shows discounting behavior converging across the marketplace. Comparing the depth and breadth of discounts for each top-level category across 2024, 2025, and 2026, two patterns stand out.

First, discount breadth has compressed broadly. Nearly every category is discounting a smaller share of its catalog than it did in 2024. Between 2024 and 2026, the share of Beauty & Personal Care products discounted fell from roughly 34.2% to 30.1%; Electronics fell from 35.4% to 26.5%; and Home & Kitchen eased from 34.1% to 27.0%. The pullback in breadth is consistent across categories, mirroring the site-wide breadth decline noted above.

Second, discount depth has converged toward a tighter band. The spread between the most- and least-discounted categories has narrowed, with most categories now clustering in the high-teens to low-twenties on average depth. Categories that ran notably deep in 2024, such as Beauty & Personal Care (33.3%) and Health & Household (30.8%), have come down closer to the pack (22.8% and 21.8% in 2026, respectively), while perennially shallow categories have moved little.

The net effect is a marketplace where discounting is both narrower and more uniform than it was two years ago. Brands looking to stand out in this environment will need to execute a more holistic strategy that prioritizes key deal visibility, deal timing based on known conversion trends, and tailoring their approach to the strength of the underlying offer relative to close competitors at the product level.

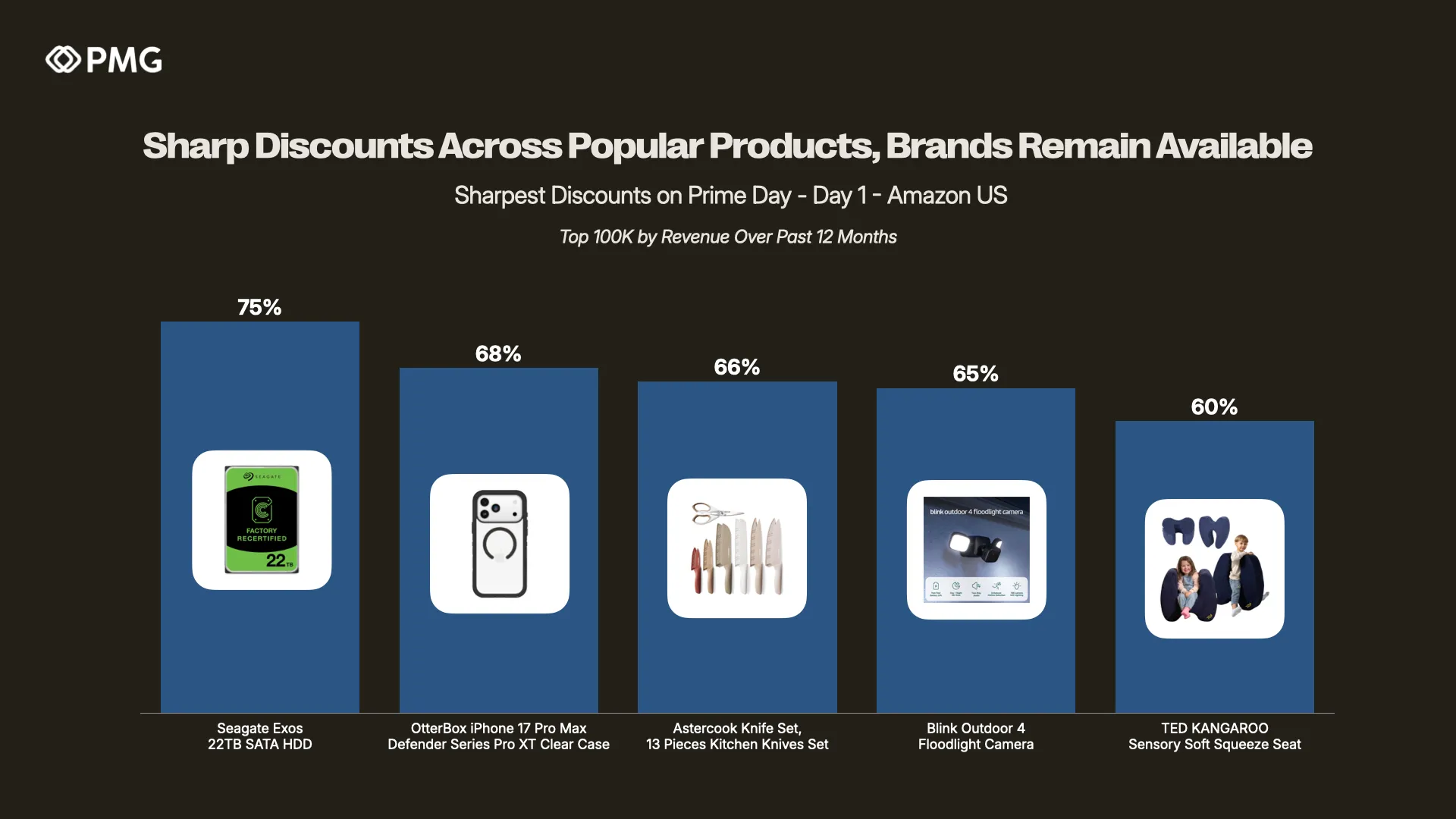

Sharp Discounts Across Popular Products, While Brands Remain Available

Even with the broader pullback in breadth, Day 1 still featured genuinely sharp discounts on high-revenue, recognizable products, highlighting how meaningful deals remain available for shoppers.

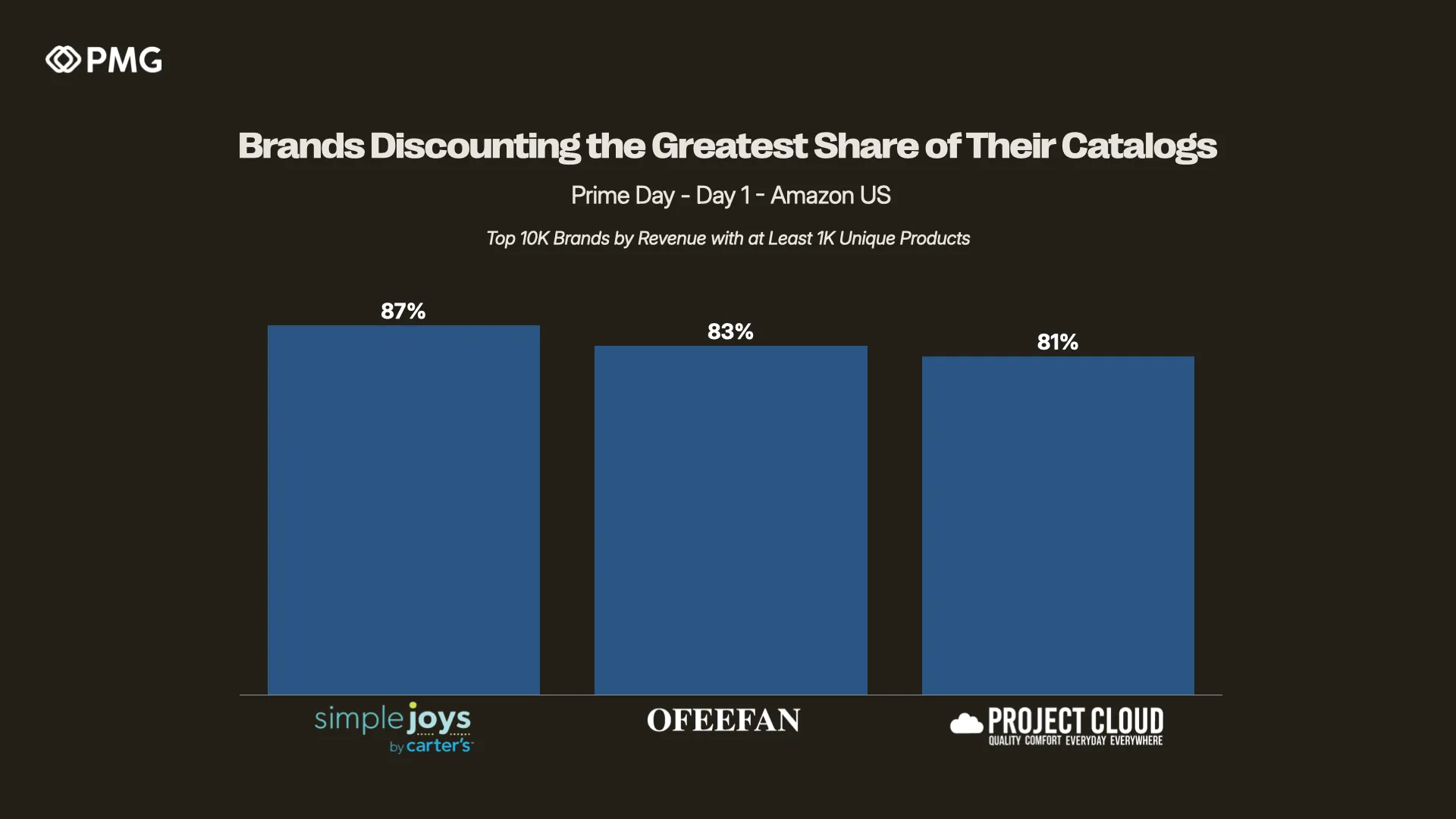

Discounting intensity also showed up at the brand level. Looking at the top 10K brands by revenue with at least 1,000 unique products, the brands discounting the greatest share of their catalogs on Day 1 were:

The presence of deep, headline-grabbing markdowns on popular electronics, accessories, and home goods, alongside brands putting the overwhelming majority of their catalogs on sale, shows that aggressive promotional strategies are still very much in play. The shift toward shallower, narrower discounting site-wide doesn't preclude standout deals, but it does make those deals more concentrated and more competitively valuable.

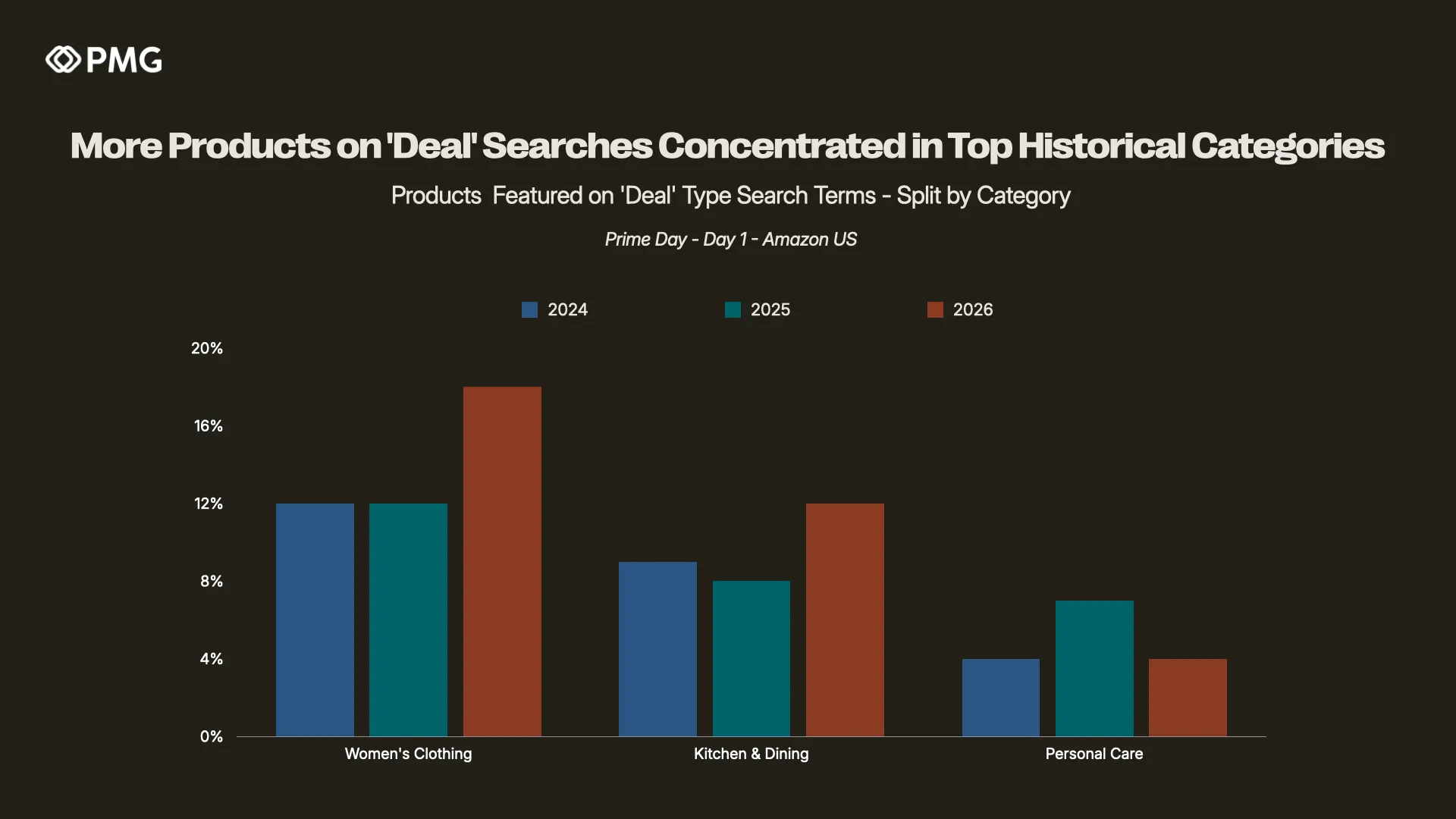

More Products on "Deal" Searches Concentrated in Top Historical Categories

Finally, the categories featured in open-ended, deal-oriented search results are growing more concentrated in the same areas that have historically anchored Prime Day.

The growing share of search results for these popular terms, concentrated in Women's Clothing and Kitchen & Dining, reinforces the point that apparel and home categories command an outsized share of deal visibility on Day 1. Like anything on Amazon, this is primarily driven by consumer behavior and conversions. For brands competing to place on these search terms, the bar for breaking through is higher.

What Brands Should Watch on Day 2 & Beyond

Shallower discounting is more pervasive, so perceived value matters more: With over a third of offers now in the 10%-19% band and deep (50%+) discounts increasingly rare, clear, comparison-friendly promotional messaging is essential to convert increasingly value-conscious shoppers.

Dive as deep as possible to contextualize competitiveness: While we provide top-level category averages in this analysis, individual brands need to go much deeper in order to drive performance. Competitive benchmarking should be done at a product-by-product level, not against the site-wide or even top category-wide average.

Standout deals still cut through: Sharp markdowns on recognizable, high-revenue products remain available, and brands willing to discount broadly are doing so. In a narrower promotional field, those moves carry more weight.

As the four-day event unfolds, PMG will continue to track how these dynamics evolve, with Day 4 looming large as the final day of Amazon sale events and historically driving the second-highest share of Prime Day purchases.