June 30, 2026

Amazon US Prime Day 2026 Full-Event Recap: A More Restrained Sale That Pulled Shoppers Into the Morning

With the four-day event now complete, a PMG analysis of tens of millions of products on Amazon US confirms the picture built over the course of Prime Day. The 2026 event was a more restrained promotional event than 2025 or 2024. Across the full event, both the depth and breadth of discounts settled below prior-year marks, the "typical" deal continued its multi-year drift toward shallower price cuts, and lighter discounting spread across nearly every top-level category. At the same time, the full-event view sharpens a behavioral shift first flagged mid-event, with shoppers pulling their buying earlier in the day, with the morning hours claiming a larger share of sales than in 2025.

This recap updates our Day 3 readout with final, full-event figures and the day-by-day trajectory that produced them.

Discount data included in this analysis encompasses both Prime Day-specific deals and general promotional discounts observed by non-logged-in users across more than 30 million products on Amazon US over the full Prime Day 2026 event. Prior year comparisons relate to the corresponding 2025 and 2024 Prime Day events, respectively.

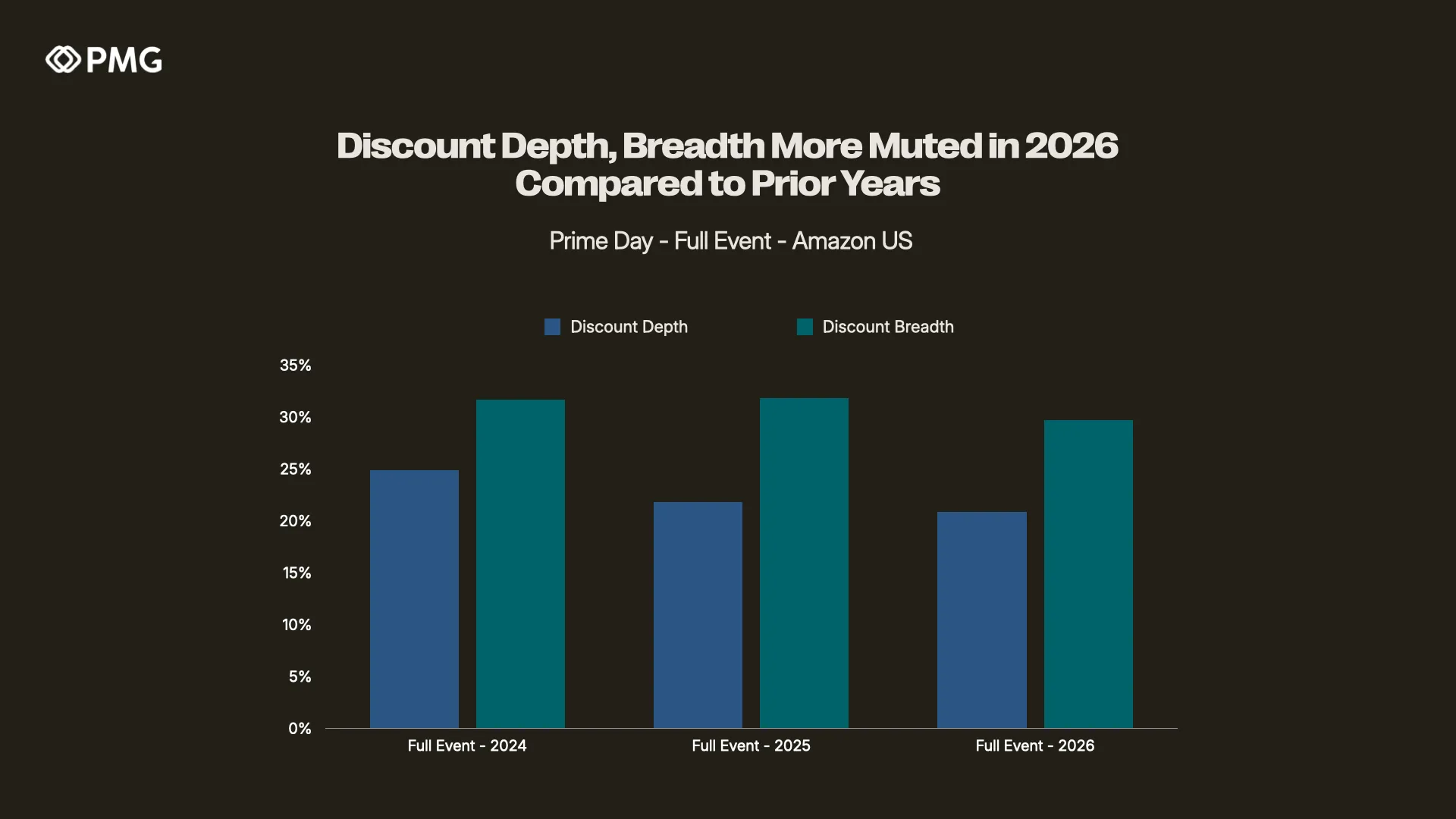

Discount Depth, Breadth More Muted in 2026 Compared to Prior Years

Across the full event, both measures of discounting landed below 2025 and well below 2024.

Discount depth: The average discount rate across the full event was 20.9%, down from 21.8% in 2025 and 24.9% in 2024, representing roughly a one-point YoY decline and nearly four points below the 2024 mark.

Discount breadth: The share of products carrying any discount was 29.7%, down from 31.8% in 2025 and 31.7% in 2024.

The day-by-day path explains how the event got there. Breadth opened soft on Day 1 (24.6%, down from 29.0% in 2025), then recovered and held through the back half — 31.6% on both Day 2 and Day 3 before easing to 31.1% on Day 4. Depth, by contrast, barely moved across all four days, sitting at 21.0%, 20.9%, 20.9%, and 21.0% on Days 1 through 4. The takeaway for brands is that the more conservative promotional posture set early in the event proved durable, with discounting never escalating as the sale wore on the way a "blowout finish" might suggest.

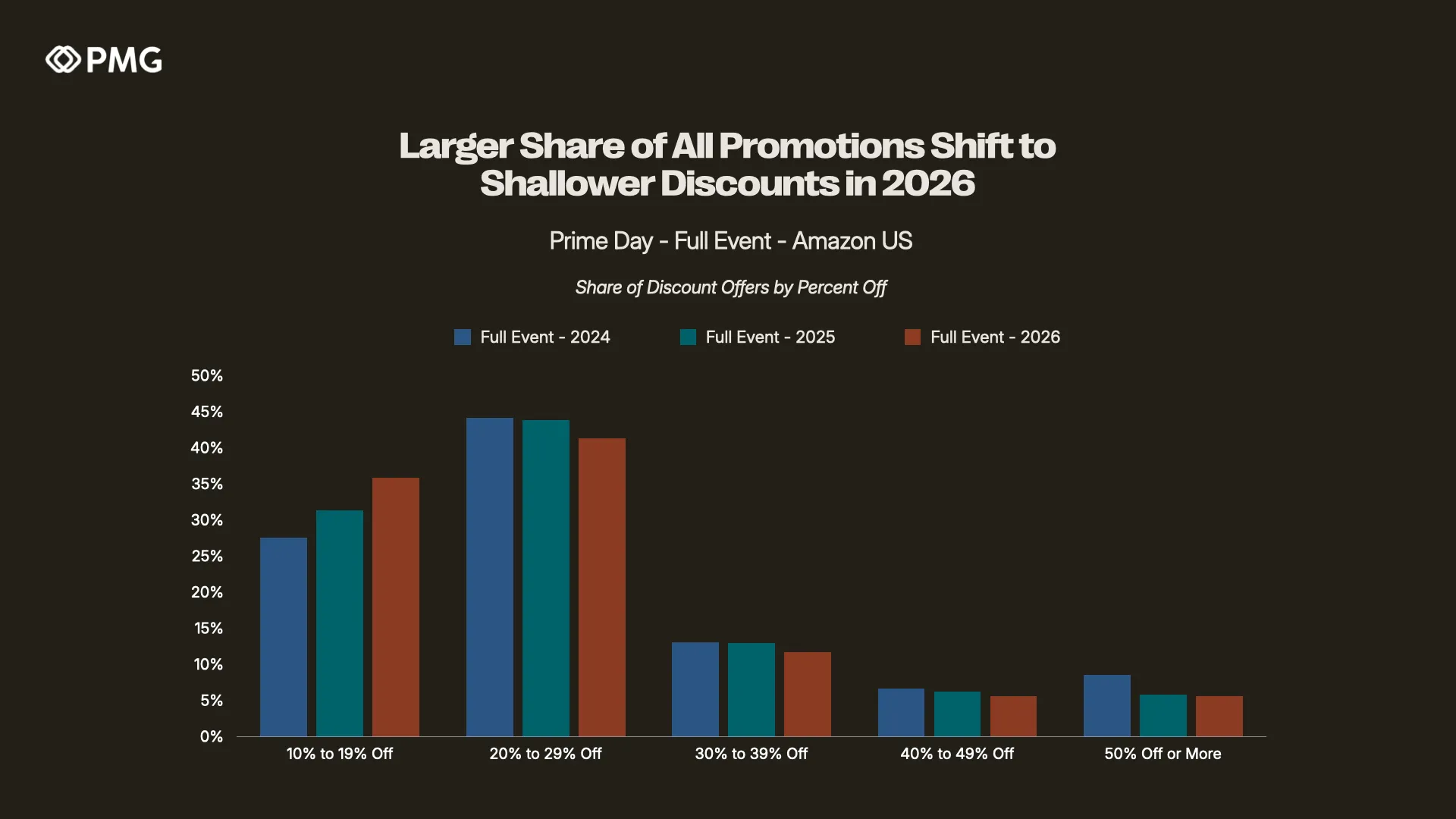

Larger Share of All Promotions Shift to Shallower Discounts in 2026

The clearest multi-year trend in the data was the distribution of discount offers by depth, which showed shallower price cuts continuing to claim a growing share of all promotions on the site.

The 10% to 19% off band climbed to 35.8% of all discount offers for the full event, up from 31.4% in 2025 and 27.6% in 2024.

The historically dominant 20% to 29% off band slipped to 41.3%, down from 43.8% in 2025 and 44.2% in 2024.

Deeper discounts continued to thin out: 30% to 39% off eased to 11.7% (from 12.9%), 40% to 49% off to 5.7% (from 6.2%), and 50% off or more to 5.6%, down from 5.8% in 2025 and 8.5% in 2024.

The pattern was remarkably consistent every single day of the event. The sub-20% band sat between 35.4% and 37.0% on each of Days 1 through 4, underscoring that this is a structural shift rather than a quirk of any one day. With "standout" markdowns less pervasive than they were even a year ago, the pressure was on many brands to better communicate and promote the value they do offer in ways beyond a big discount figure.

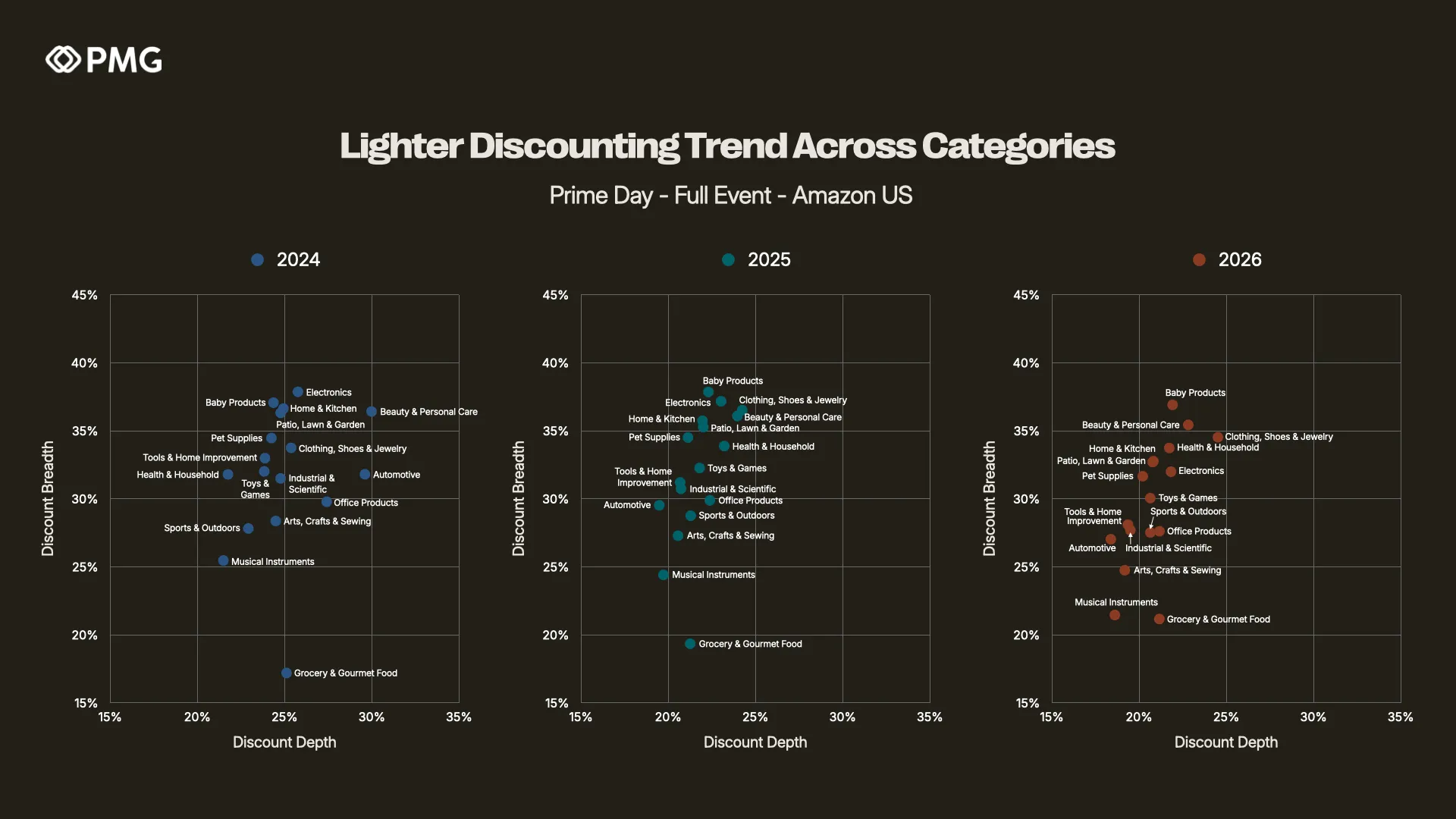

Lighter Discounting Trend Across Categories

Looking beyond whole-site averages, the full-event category grid shows the lighter discounting evident at the marketplace level broadening across nearly all of Amazon US.

Depth eased in every top-level category. The steepest pullbacks came in Health & Household (23.2% → 21.7%), Beauty & Personal Care (24.0% → 22.8%), and Office Products (22.4% → 21.2%). Even the most aggressively discounted category, Clothing, Shoes & Jewelry, held average depth essentially flat at 24.5% (vs. 24.2% in 2025), keeping it the deepest-discounting category on the site.

Breadth compressed in most categories but not all. Automotive (29.5% → 27.0%) and Tools & Home Improvement (31.2% → 28.1%) saw the largest declines in the share of products on deal. Running counter to the trend, Clothing, Shoes & Jewelry (33.8% → 34.5%) and Grocery & Gourmet Food (19.4% → 21.2%) actually widened their discounting footprint year over year.

The net effect is a marketplace where lighter discounting is no longer confined to a few categories but is increasingly the norm across the board. For brands, that makes category-level benchmarking less useful in isolation. Standing out increasingly depends on understanding relative competitiveness at the product level rather than against a broad category average.

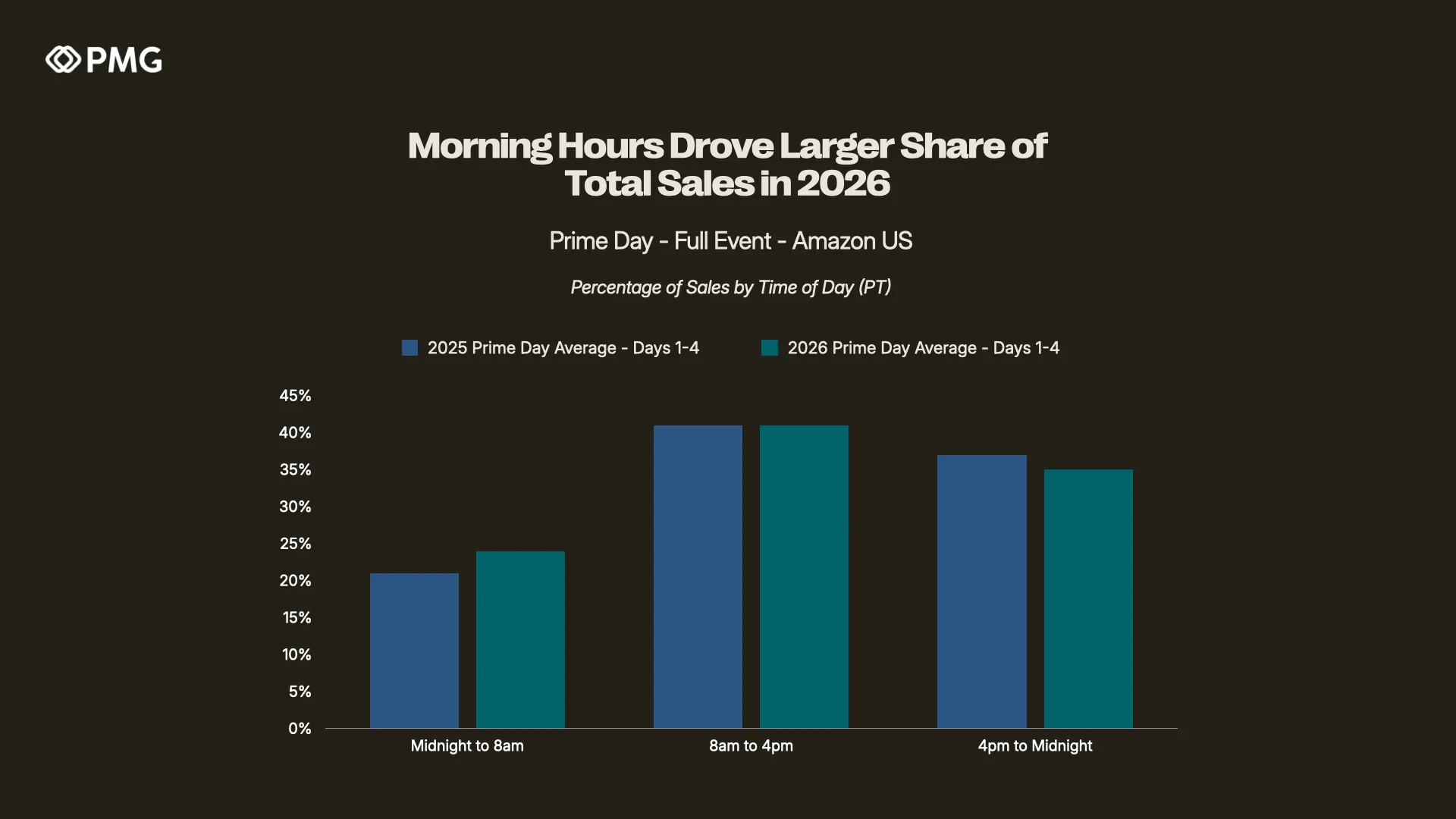

Morning Hours Drove Larger Share of Total Sales in 2026

The full-event view confirms the behavioral shift that surfaced mid-event, with the distribution of sales by time of day consistently moving earlier compared with 2025.

The midnight-to-8am window captured 23.7% of sales in 2026, up from 21.4% in 2025, a gain of more than two percentage points.

The 8am-to-4pm window held essentially flat at 41.3% (vs. 41.2% in 2025).

The 4pm-to-midnight window slipped to 35.0%, down from 37.4% in 2025, a decline of about 2.4 points.

In other words, overall demand over the event was weighted much more towards the morning hours, rather than ‘prime time’, which has traditionally been a strong period during the event. For brands and advertisers, that has direct implications for budget pacing and dayparting. With the conversion opportunity skewing earlier, strategies built around an evening surge need to shift to account for more demand arriving earlier in the day.

Takeaways for Brands Heading Out of Prime Day 2026

The full-event data reinforces a clear theme in terms of a shallower promotional event, paired with a meaningful shift in when shoppers transacted. A few implications for brands as we enter Q3 and upcoming high traffic periods like back-to-school and Prime Big Deal Days:

Plan for a shallower discount baseline. With full-event average discount depth at 20.9% and the sub-20%-off band now the fastest-growing tier of all promotions, brands can be more strategic around when and where to apply steeper discounts.

Rebuild dayparting around an earlier curve. With the morning gaining share and the evening shedding it YoY, bid and budget pacing concentrated in the back half of the day risks underweighting the windows where demand is actually settling.

Contextualize competitiveness at the product level. As lighter discounting spreads across more categories, broad category averages reveal less about how a given product stacks up. A product-by-product view of relative pricing against direct competitors on the search page remains the clearest guide to where a deal will actually break through.

Next week we’ll provide additional readouts of Prime Day 2026 activity in terms of sales, and overall retail impact beyond Amazon US, to give brands an even deeper understanding of the implications of this latest sale event on Q3 and beyond.